Why Does A Hard Inquiry Hurt Your Credit? Understanding The Impact

Have you ever wondered why does a hard inquiry hurt your credit? If you're planning to apply for a loan or credit card, understanding the effects of hard inquiries on your credit score is crucial. Hard inquiries can impact your financial standing and must be managed carefully.

Managing your credit score is an essential part of maintaining financial health. Hard inquiries are one of the factors that can affect your credit score, and it's important to understand their role in the broader context of credit management.

This article will explore the reasons behind why hard inquiries hurt your credit, how much they can affect your score, and what steps you can take to minimize their impact. By the end of this article, you'll have a comprehensive understanding of hard inquiries and their implications.

Read also:Barclays Center 620 Atlantic Ave Brooklyn New York 11217 A Comprehensive Guide

Table of Contents

- What is a Hard Inquiry?

- How Do Hard Inquiries Affect Credit Scores?

- Difference Between Hard and Soft Inquiries

- How Long Do Hard Inquiries Stay on Your Credit Report?

- How Much Does a Hard Inquiry Hurt Your Credit?

- The Impact of Hard Inquiries on Credit Score

- Avoiding Multiple Hard Inquiries

- Strategies to Manage Credit Inquiries

- Credit Monitoring Tools and Resources

- Final Thoughts: Why Does a Hard Inquiry Hurt Your Credit?

What is a Hard Inquiry?

A hard inquiry occurs when a lender checks your credit report as part of a loan or credit application process. This type of inquiry is typically initiated by you, the consumer, and reflects a formal request for credit. Hard inquiries are recorded on your credit report and can impact your credit score.

When Do Hard Inquiries Occur?

Hard inquiries happen when you apply for various types of credit, including:

- Mortgage loans

- Auto loans

- Credit cards

- Personal loans

- Student loans

These inquiries are an important part of the credit evaluation process, as they indicate that you are actively seeking new credit.

How Do Hard Inquiries Affect Credit Scores?

Hard inquiries can have a direct impact on your credit score. Credit scoring models, such as FICO and VantageScore, consider the number of hard inquiries as one of the factors when calculating your score. While the effect is usually minimal, repeated inquiries can add up and lead to a more significant impact over time.

Read also:Splashtown Usa San Antonio The Ultimate Water Adventure For Your Family

Factors That Influence the Impact

The extent to which a hard inquiry affects your credit score depends on several factors:

- The number of recent hard inquiries

- Your overall credit history and credit utilization

- The type of credit you're applying for

For individuals with shorter credit histories, the impact of hard inquiries may be more pronounced.

Difference Between Hard and Soft Inquiries

It's important to distinguish between hard inquiries and soft inquiries. While both involve checking your credit report, they differ in their impact on your credit score:

Hard Inquiries

Hard inquiries are initiated by lenders when you apply for credit. They are recorded on your credit report and can affect your credit score.

Soft Inquiries

Soft inquiries occur when you or others check your credit report for non-lending purposes. Examples include checking your own credit score, pre-approved credit offers, and employment background checks. Soft inquiries do not affect your credit score.

How Long Do Hard Inquiries Stay on Your Credit Report?

Hard inquiries remain on your credit report for two years. However, most credit scoring models only consider hard inquiries from the past 12 months when calculating your credit score. This means that while inquiries may stay on your report for two years, their impact diminishes over time.

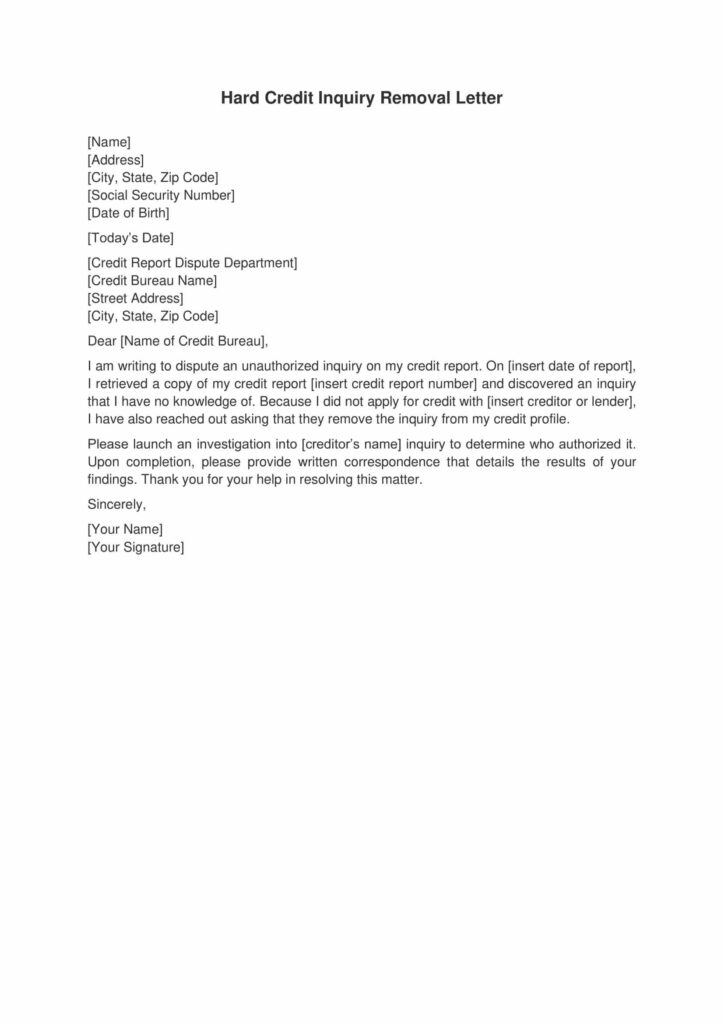

Can You Remove Hard Inquiries?

In some cases, you may be able to dispute and remove unauthorized hard inquiries from your credit report. If an inquiry was made without your consent, you can contact the credit bureau to initiate a dispute.

How Much Does a Hard Inquiry Hurt Your Credit?

The impact of a hard inquiry on your credit score varies depending on your individual credit profile. On average, a single hard inquiry can lower your credit score by 5 to 10 points. However, the effect is typically short-lived, and your score can recover as long as you maintain responsible credit behavior.

Factors That Affect the Impact

Several factors can influence how much a hard inquiry affects your credit score:

- Your credit history length

- Number of existing credit accounts

- Recent credit applications

- Credit utilization ratio

For individuals with strong credit histories, the impact of a single hard inquiry may be negligible.

The Impact of Hard Inquiries on Credit Score

Hard inquiries contribute to the "new credit" category in credit scoring models, which accounts for approximately 10% of your overall credit score. This category evaluates how often you apply for new credit and the potential risk associated with it.

Why Are Hard Inquiries Important?

Lenders use hard inquiries as a signal of credit-seeking behavior. Frequent hard inquiries may indicate financial instability or a higher risk of default, which can lead to a lower credit score. However, occasional inquiries are generally not a cause for concern.

Avoiding Multiple Hard Inquiries

Applying for multiple credit accounts within a short period can result in multiple hard inquiries, which can negatively impact your credit score. To avoid this, consider the following strategies:

- Shop around for credit within a short time frame (e.g., 14 days) to minimize the impact of multiple inquiries.

- Pre-qualify for credit offers to gauge your eligibility before applying.

- Limit unnecessary credit applications to reduce the number of hard inquiries.

Rate Shopping and Credit Inquiries

When shopping for loans, such as mortgages or auto loans, multiple inquiries within a short period (usually 14-45 days) are often treated as a single inquiry by credit scoring models. This allows you to compare rates without significantly impacting your credit score.

Strategies to Manage Credit Inquiries

Managing credit inquiries effectively is key to maintaining a healthy credit score. Here are some strategies to help you minimize the impact of hard inquiries:

- Monitor your credit report regularly to identify unauthorized inquiries.

- Only apply for credit when necessary and ensure you meet the eligibility criteria.

- Use credit monitoring tools to track changes in your credit score.

Building a Strong Credit History

A strong credit history can help mitigate the impact of hard inquiries. Focus on paying bills on time, maintaining low credit utilization, and managing your existing credit accounts responsibly.

Credit Monitoring Tools and Resources

Several credit monitoring tools and resources can help you stay informed about your credit score and credit inquiries:

- Credit bureaus like Experian, Equifax, and TransUnion offer free credit reports annually.

- Personal finance apps and credit monitoring services provide real-time updates on your credit score and activity.

- Financial advisors and credit counselors can offer guidance on managing credit inquiries and improving your credit health.

Why Is Credit Monitoring Important?

Credit monitoring allows you to track changes in your credit report and identify potential issues, such as unauthorized inquiries or errors. By staying informed, you can take proactive steps to protect your credit score and financial well-being.

Final Thoughts: Why Does a Hard Inquiry Hurt Your Credit?

In conclusion, hard inquiries can impact your credit score, but their effect is generally minimal and short-lived. By understanding how hard inquiries work and implementing strategies to manage them, you can maintain a healthy credit score and financial standing.

Take Action: To improve your credit health, regularly monitor your credit report, limit unnecessary credit applications, and focus on responsible credit management. Share this article with others who may benefit from understanding the impact of hard inquiries on credit scores.

For more insights on credit management and financial wellness, explore our other articles and resources. Your financial future starts today!

Source: Consumer Financial Protection Bureau

{kind=link}